Understanding Uninsured Motorist Coverage

An explanation of uninsured and underinsured motorist coverage and its importance.

An explanation of uninsured and underinsured motorist coverage and its importance.

Understanding Uninsured Motorist Coverage

Hey there, ever wondered what happens if you get into a car accident and the other driver doesn't have insurance? Or worse, they have some insurance, but it's not enough to cover all your damages? It's a scary thought, right? That's where Uninsured Motorist (UM) and Underinsured Motorist (UIM) coverage comes into play. These aren't just fancy terms; they're crucial protections that can save you a ton of headaches and financial strain. Let's dive deep into what these coverages are, why they're so important, and how they work, especially for drivers in the US and Southeast Asia.

What is Uninsured Motorist Coverage UM Explained

So, what exactly is Uninsured Motorist (UM) coverage? Simply put, it's a part of your car insurance policy that protects you if you're involved in an accident with a driver who doesn't have any car insurance at all. Think about it: if an uninsured driver hits you, who pays for your medical bills, lost wages, and car repairs? Without UM coverage, you might be stuck footing those bills yourself, or you'd have to sue the at-fault driver, which can be a long, expensive, and often fruitless process if they don't have assets. UM coverage steps in to cover these costs, just as if the at-fault driver had insurance.

Types of Uninsured Motorist Coverage UM Bodily Injury and UM Property Damage

UM coverage usually comes in two main flavors: Uninsured Motorist Bodily Injury (UMBI) and Uninsured Motorist Property Damage (UMPD).

- UM Bodily Injury (UMBI): This is probably the most critical part. UMBI covers medical expenses, lost wages, pain and suffering, and other costs related to injuries you and your passengers sustain in an accident caused by an uninsured driver. It's designed to cover what the at-fault driver's liability insurance would have paid if they had it.

- UM Property Damage (UMPD): As the name suggests, UMPD covers the damage to your vehicle if an uninsured driver hits you. This can include repair costs or the actual cash value of your car if it's totaled. However, it's worth noting that some states might not offer UMPD, or it might have a deductible, similar to your collision coverage. In some cases, your collision coverage might also cover damage from an uninsured driver, but then you'd pay your collision deductible.

What is Underinsured Motorist Coverage UIM Explained

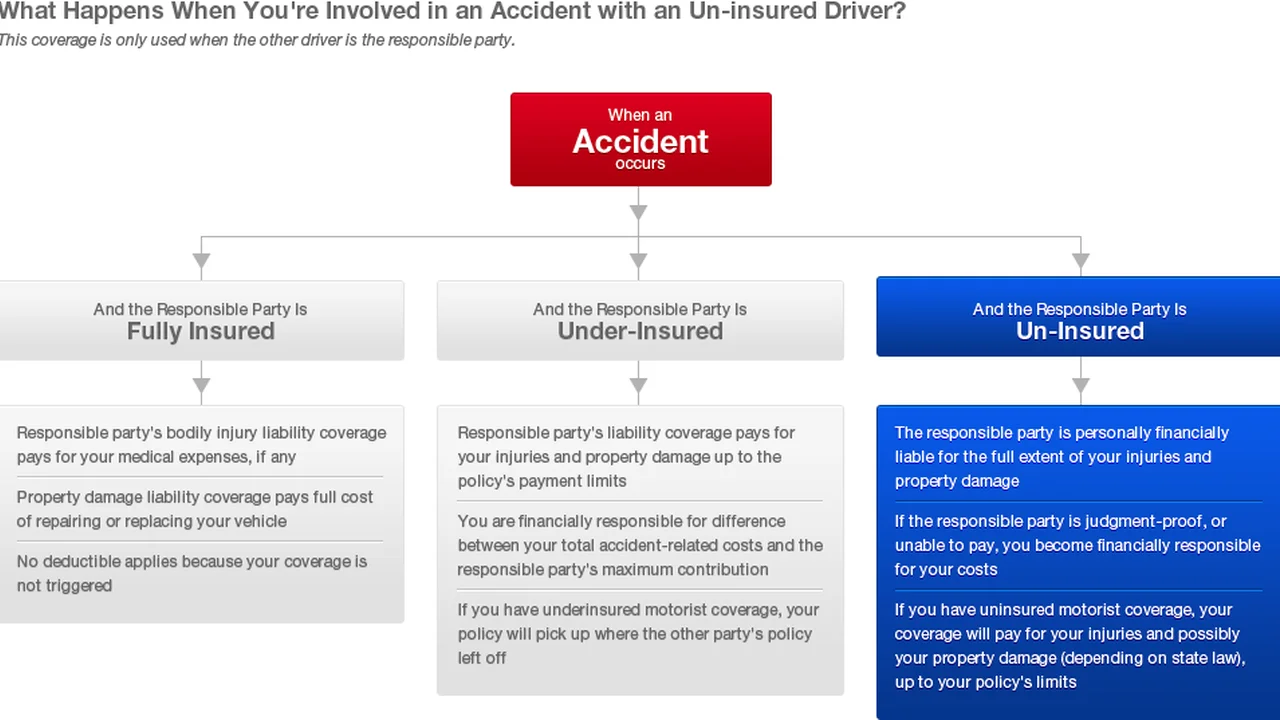

Now, let's talk about Underinsured Motorist (UIM) coverage. This is equally important because it addresses a slightly different, but very common, scenario. UIM coverage protects you when the at-fault driver does have insurance, but their liability limits aren't high enough to cover all your damages. Imagine you're in a serious accident, and your medical bills alone are $100,000, but the at-fault driver only has a $25,000 bodily injury liability limit. That leaves a huge gap! UIM coverage kicks in to cover the difference, up to your policy's UIM limits.

How UIM Coverage Works Bridging the Gap

The way UIM works can sometimes be a bit confusing, but the core idea is simple: it fills the gap. If the other driver's insurance pays out its maximum, and your damages are still higher, your UIM coverage will pay the remainder, up to your UIM policy limits. It's like having an extra layer of protection for those situations where the other driver's insurance just isn't enough.

Why UM and UIM Coverage are Essential Protecting Your Financial Future

You might be thinking, "Do I really need this?" The answer, especially in today's world, is a resounding YES. Here's why UM and UIM coverage are absolutely essential:

High Rates of Uninsured Drivers in the US and Southeast Asia

Unfortunately, the number of uninsured drivers on the road is higher than you might think. In the US, some states have a significant percentage of uninsured motorists. For example, states like Florida, Mississippi, and New Mexico often report higher rates. This means there's a real chance you could encounter an uninsured driver. In Southeast Asia, while regulations vary by country, enforcement can sometimes be a challenge, and the prevalence of uninsured or underinsured drivers can also be a concern, especially in rapidly developing urban areas with diverse vehicle types.

Rising Medical Costs and Vehicle Repair Expenses

Let's face it, medical care isn't cheap, and neither are car repairs, especially with modern vehicles packed with advanced technology. A serious accident can quickly lead to tens of thousands of dollars in medical bills, not to mention the cost of repairing or replacing your car. Without UM/UIM, these costs could fall squarely on your shoulders, potentially leading to bankruptcy or severe financial hardship.

Protection for You and Your Passengers Comprehensive Coverage

UM/UIM coverage isn't just for your car; it's primarily for you and your passengers. It covers your medical bills, lost wages if you can't work, and even pain and suffering. This means that even if you have health insurance, UMBI can cover deductibles, co-pays, and other expenses that health insurance might not, or it can act as primary coverage if your health insurance has high limits or exclusions for auto accidents.

Avoiding Lengthy Legal Battles Peace of Mind

Imagine getting into an accident, being injured, and then having to spend months or even years in court trying to get compensation from an uninsured driver who might not have any assets. It's a nightmare. UM/UIM coverage allows you to deal directly with your own insurance company, which is generally a much smoother and faster process, providing you with much-needed peace of mind during a stressful time.

How Much UM and UIM Coverage Do You Need Determining Adequate Protection

This is a critical question. While some states require UM/UIM coverage, others don't, or they only require minimal amounts. It's generally recommended to carry UM/UIM limits that match your bodily injury liability limits. So, if you have $100,000/$300,000 in liability coverage, you should aim for the same for your UM/UIM. Why? Because if you're responsible for an accident, you want to be able to cover the other party's damages. If someone else is responsible for your damages, you'd want the same level of protection for yourself.

Factors to Consider When Choosing Limits Your Financial Situation and Risk Tolerance

- Your Assets: If you have significant assets (a home, savings, investments), you'll want higher UM/UIM limits to protect them from potential medical bills and lost income.

- Your Income: If you rely heavily on your income and would be severely impacted by lost wages due to an injury, higher UMBI limits are crucial.

- Medical Expenses: Consider the potential cost of medical treatment for serious injuries. Even with health insurance, deductibles and co-pays can add up quickly.

- Cost of Coverage: UM/UIM coverage is often relatively inexpensive compared to the protection it offers. Get quotes for different limits to see what fits your budget.

UM and UIM Coverage in the US State Specific Regulations

In the United States, UM and UIM laws vary significantly from state to state. Some states mandate that insurance companies offer UM/UIM coverage, and you have to actively reject it in writing if you don't want it. Other states make it optional. It's crucial to understand your state's specific requirements and recommendations.

Examples of State Requirements and Recommendations

- Mandatory States: Some states, like Maryland and New York, require drivers to carry UM/UIM coverage.

- Optional States: In states like Florida, UM/UIM is optional, but highly recommended due to the high percentage of uninsured drivers.

- "Stacking" vs. "Non-Stacking": This is an important concept. In some states, you can "stack" your UM/UIM coverage, meaning if you have multiple vehicles insured on the same policy, you can multiply your UM/UIM limits by the number of vehicles. For example, if you have $50,000 UMBI and two cars, you might have $100,000 in stacked coverage. Other states are "non-stacking," meaning your limits apply per accident, regardless of how many cars you insure.

UM and UIM Coverage in Southeast Asia Regional Considerations

The automotive insurance landscape in Southeast Asia is diverse, with each country having its own regulations and market conditions. While the concept of UM/UIM might not always be explicitly named as such in every country's standard policy, similar protections often exist or can be added.

Country Specific Examples and Best Practices

- Thailand: Compulsory Motor Insurance (CMI) covers basic bodily injury for all parties, but limits are often low. Voluntary insurance policies, particularly comprehensive ones, often include personal accident coverage for the driver and passengers, which can act similarly to UMBI. It's crucial to check policy wordings for coverage against uninsured third parties.

- Malaysia: Third-party motor insurance is mandatory. Comprehensive policies offer broader protection. While specific UM/UIM clauses might not be standard, many comprehensive policies offer personal accident benefits and can be extended to cover damage from uninsured drivers, often through specific add-ons or endorsements.

- Indonesia: Mandatory third-party liability insurance is not as widespread as in some other countries. Comprehensive insurance is highly recommended. Some insurers offer extensions for personal accident coverage and specific clauses for damage caused by unidentified or uninsured vehicles, which function similarly to UM/UIM.

- Philippines: Compulsory Third Party Liability (CTPL) is mandatory but has very low limits. Comprehensive policies are essential. Many insurers offer "Uninsured Motorist" or "Personal Accident" riders that provide similar benefits to UM/UIM, covering medical expenses and sometimes property damage if the at-fault party is uninsured or cannot be identified.

- Vietnam: Mandatory civil liability insurance covers third-party bodily injury and property damage, but limits are often low. Voluntary comprehensive insurance is available and often includes personal accident coverage. Specific UM/UIM provisions might be less common as standalone features but can be covered under broader personal accident or all-risk clauses.

Recommendation for Southeast Asia: When purchasing insurance in Southeast Asia, it's vital to discuss with your insurer or agent the specific protections available for accidents involving uninsured or underinsured drivers. Look for policies that offer robust personal accident coverage for yourself and your passengers, and inquire about extensions or riders that cover damage to your vehicle when the at-fault party is uninsured or unidentifiable. Always read the policy wording carefully and ask for clarification on how such scenarios are handled.

Comparing UM and UIM with Other Coverages Understanding the Differences

It's easy to get confused with all the different types of car insurance. Let's quickly compare UM/UIM with some other common coverages to highlight their unique role.

UM UIM vs Collision Coverage Property Damage Protection

Collision coverage pays for damage to your car if you hit another car or object, or if your car rolls over, regardless of who is at fault. UMPD specifically covers damage to your car when an uninsured driver is at fault. If you have collision coverage, it will typically cover damage from an uninsured driver, but you'll pay your collision deductible. UMPD might have a lower or no deductible in some cases, making it a good complement.

UM UIM vs Medical Payments MedPay or Personal Injury Protection PIP Injury Protection

MedPay and PIP cover medical expenses for you and your passengers, regardless of fault. They are often primary coverage for medical bills up to their limits. UMBI, however, specifically covers injuries when an uninsured or underinsured driver is at fault, and it can also cover lost wages and pain and suffering, which MedPay/PIP typically do not. UMBI often kicks in after MedPay/PIP limits are exhausted or if you don't have those coverages.

UM UIM vs Health Insurance Comprehensive Health Coverage

While your health insurance will cover your medical bills, it might not cover all accident-related expenses like lost wages or pain and suffering. Also, health insurance might have high deductibles or co-pays, and some policies might even have subrogation clauses, meaning they can seek reimbursement from any settlement you receive from an auto accident. UMBI can help cover these gaps and protect your health insurance from being the sole payer for accident-related medical costs.

Filing a Claim with UM or UIM Coverage Step by Step Process

If you find yourself in an accident with an uninsured or underinsured driver, here's a general idea of how the claims process typically works:

- Report the Accident: Immediately report the accident to the police and your insurance company. Get a police report, as it's crucial for your claim.

- Gather Information: Collect as much information as possible from the other driver, even if they claim to be uninsured. Get their name, contact info, and vehicle details. If they flee, note down their vehicle description and license plate if possible.

- Seek Medical Attention: If you're injured, get medical attention right away. Your health and well-being are paramount.

- Notify Your Insurer: Inform your insurance company that the other driver is uninsured or underinsured. They will guide you through the specific steps for filing a UM/UIM claim.

- Provide Documentation: You'll need to provide documentation of your injuries, medical bills, lost wages, and vehicle damage.

- Negotiation and Settlement: Your insurance company will investigate the claim and negotiate a settlement with you, similar to how they would if they were paying out a claim to a third party.

Specific Product Recommendations and Considerations Choosing the Right Policy

While I can't recommend specific insurance policies as I'm an AI and not a licensed insurance agent, I can give you some general advice on what to look for and how to compare options. The best "product" here is a well-structured policy from a reputable insurer.

Top Insurance Providers in the US for UM UIM Coverage

When looking for UM/UIM coverage in the US, consider major insurers known for their customer service and financial stability. These companies generally offer robust UM/UIM options:

- State Farm: Often praised for its extensive agent network and personalized service. They offer competitive UM/UIM options and are known for handling claims efficiently.

- GEICO: A popular choice for online convenience and often competitive pricing. Their UM/UIM coverage is straightforward to add to policies.

- Progressive: Known for innovative tools and discounts. Progressive offers strong UM/UIM options and can be a good fit for drivers looking for comprehensive coverage.

- Allstate: Offers a wide range of coverage options and local agents. Allstate's UM/UIM can be customized to fit various needs.

- Farmers: Provides personalized service through agents and offers various policy options, including robust UM/UIM.

Usage Scenario: If you live in a state with a high percentage of uninsured drivers (e.g., Florida, Mississippi), prioritizing higher UMBI limits with any of these providers is crucial. If you frequently drive in areas with heavy traffic or where minor accidents are common, consider adding UMPD or ensuring your collision deductible is manageable.

Key Considerations for Southeast Asian Markets UM UIM Equivalents

In Southeast Asia, as discussed, the terminology might differ, but the need for protection remains. When speaking with local insurers, inquire about:

- Personal Accident (PA) Coverage: This is often a standalone or add-on feature that covers medical expenses and sometimes disability/death for the driver and passengers, regardless of fault. It's the closest equivalent to UMBI for your injuries.

- Extensions for Unidentified or Uninsured Vehicles: Ask if your comprehensive policy can be extended to cover damage to your vehicle if the at-fault party is uninsured or flees the scene. This acts like UMPD.

- Higher Third-Party Liability Limits: While not directly UM/UIM, opting for higher third-party liability limits on your own policy is a good practice. It shows you're a responsible driver and can sometimes influence how your insurer views your overall risk profile.

Example Insurers (General, check local availability):

- AXA: A global insurer with a strong presence in many Southeast Asian countries, offering various comprehensive motor insurance plans.

- MSIG: Another prominent international insurer in the region, known for its diverse product offerings.

- Local National Insurers: Companies like Bangkok Insurance (Thailand), Etiqa (Malaysia), or Prudential (various countries) often have tailored products for their local markets.

Usage Scenario: For drivers in bustling cities like Bangkok, Jakarta, or Manila, where traffic can be chaotic and the risk of minor collisions is higher, ensuring robust PA coverage and property damage protection against uninsured drivers is paramount. If you frequently travel between countries, ensure your policy offers adequate cross-border coverage or consider travel insurance that includes motor accident benefits.

Comparing Costs and Value Getting Quotes and Discounts

The cost of UM/UIM coverage is usually a small fraction of your overall premium, but it offers immense value. Always get quotes from multiple providers. Look for discounts that can lower your overall premium, such as:

- Bundling: Combining auto and home insurance.

- Good Driver Discounts: For maintaining a clean driving record.

- Multi-Car Discounts: Insuring multiple vehicles with the same company.

- Safety Features: Discounts for cars with advanced safety features.

- Defensive Driving Courses: Completing approved courses.

Pricing Example (US, illustrative only): For a typical driver with a clean record, adding UM/UIM coverage with limits matching their liability (e.g., $100,000/$300,000) might add anywhere from $50 to $200 per year to their premium, depending on the state, insurer, and other factors. This small additional cost is a tiny price to pay for potentially hundreds of thousands of dollars in protection.

Pricing Example (Southeast Asia, illustrative only): For comprehensive policies in Southeast Asia, the cost of adding personal accident riders or extensions for uninsured vehicle damage might range from an additional 5% to 15% of the base premium, depending on the limits chosen and the specific country's market. Again, this is a small investment for significant peace of mind.

Common Misconceptions About UM and UIM Clarifying the Details

Let's clear up a few common misunderstandings about UM/UIM coverage:

- "My health insurance will cover everything": As discussed, health insurance might not cover all accident-related costs, especially lost wages or pain and suffering, and might have high deductibles.

- "I have collision, so I don't need UMPD": While collision covers damage from an uninsured driver, UMPD might have a lower deductible or no deductible, saving you money out-of-pocket.

- "It's only for uninsured drivers": Remember, UIM also protects you from drivers who have some insurance, but not enough.

- "It's too expensive": Compared to the potential costs of an accident with an uninsured driver, UM/UIM is typically a very affordable and high-value coverage.

The Future of UM and UIM Coverage Adapting to New Mobility

As the automotive industry evolves with electric vehicles, autonomous driving, and new mobility services like ride-sharing, UM/UIM coverage will also need to adapt. Insurers are constantly reviewing and updating their policies to address these new risks.

UM UIM in the Age of Ride Sharing and Autonomous Vehicles

For ride-sharing drivers, specific ride-sharing insurance policies often include UM/UIM components to cover the unique risks associated with transporting passengers. For autonomous vehicles, the question of fault in an accident becomes more complex, potentially shifting liability to manufacturers or software providers, which could influence the future structure of UM/UIM.

Ultimately, Uninsured and Underinsured Motorist coverage isn't just another line item on your insurance bill; it's a fundamental safeguard for your financial well-being. In a world where not everyone plays by the rules, or where even responsible drivers might not carry enough insurance, UM/UIM ensures that you and your loved ones are protected. Take the time to understand your options, choose adequate limits, and drive with confidence, knowing you're covered no matter what the road throws your way.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)